This article combines the article by Fu Jun, the president of the Macau International Design Federation. Although the article was written in 2023 and does not supplement the latest information, it has considerable value for understanding the overview of the Philippine gaming industry to a certain extent.

Introduction

The Philippines, as a country where the gaming industry has developed rapidly in recent years, has promising future growth potential. However, due to its significant overlap with Macau in terms of customer sources and its pioneering and breakthrough policy exploration, regional competition will become more intense. However, information about the Philippine gaming industry is mostly scattered across new media and lacks systematic organization. Although there is a wealth of information on the internet, it is still not detailed enough.

In terms of industry data and statistics, PAGCOR, as the regulatory body of the gaming industry, does not provide very comprehensive reports. The descriptions therein are inconsistent, lacking in detail and accounting methods, making it difficult to study the Philippine gaming industry.

The purpose of this article is to organize and collect the current fragmented information, focus on sorting out and analyzing the development context and current situation of the Philippine gaming industry, and form a comprehensive understanding of the Philippine gaming industry as much as possible. On this basis, study its future development trends. Finally, it will be compared and analyzed with the Macau gaming industry to provide references for the development of the Macau gaming industry.

1. Introduction to the Philippine Gaming Industry

1.1 History of the Philippine Gaming Industry

The history of gambling in the Philippines can be traced back to the 18th century, initially as a folk entertainment activity. Subsequently, the Spanish colonial authorities gradually introduced activities such as lotteries and horse racing, and experimentally established small casinos, making gambling activities in the Philippines increasingly prosperous. In 1930, under the promotion and supervision of the American colonial authorities, gambling began to be legalized for charitable purposes. This not only increased government revenue but also solved some social employment problems at the time. After the independence of the Philippines in 1946, the new government began to be responsible for supervising and managing gambling activities nationwide.

By 1976, in order to stop the spread of illegal casino operations nationwide, then Philippine President Ferdinand Marcos issued a presidential decree to establish the state-controlled Philippine Amusement and Gaming Corporation (PAGCOR, hereinafter referred to as PAGCOR), to regulate and manage existing physical casinos. In 2003, the First Cagayan Leisure and Resort Corporation issued the first offshore gaming license, marking the beginning of legal offshore gaming.

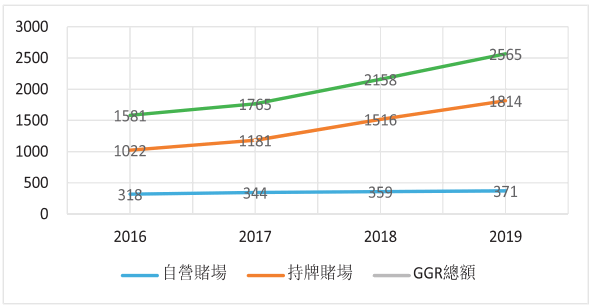

Gross gaming revenue is an important data that visually demonstrates the development of the gaming industry. Through PAGCOR's statistics, it can be seen that from 2012 to 2019, before the outbreak of the COVID-19 pandemic, the gross gaming revenue in the Philippines was approximately 84.7 billion, 95.3 billion, 116.4 billion, 130 billion, 158.1 billion, 176.5 billion, 215.8 billion, and 256.4 billion pesos respectively. Over these eight years, the total gaming revenue in the Philippines showed continuous growth, reaching a historical peak in 2019, three times that of its 2012 gross gaming revenue.

In 2017, Fitch Ratings, one of the world's three major rating agencies, released the "Eye in the Sky Series: Philippines (Gaming Jurisdiction Surveillance Monitor)" report, which pointed out, "Despite intense competition in the Asian region, the Philippine gaming industry still maintains a significant advantage with a promising outlook. Although its total GGR (Gross Gaming Revenue) is still less than Macau, the growth trend is still leading in the surrounding regions during the same period."

1.2 Economic Status of the Gaming Industry in the Philippines

In recent years, the overall economic development trend of the Philippines has been good, with GDP showing a steady upward trend. According to data from the World Bank and the IMF, the Philippines has been ranked fourth in ASEAN since 2015, surpassed Singapore to rise to third in ASEAN in 2019-2020, and the GDP growth rate in the first three quarters of 2022 was 7.7%, temporarily ranking third in ASEAN.

As an emerging economy, the second and third industries in the Philippines have relatively stable shares of GDP, with little fluctuation. Through the analysis of historical data from the MacroMicro website, the third industry in the Philippines accounts for about 60% of its GDP. As a sub-sector under the third industry, the gaming industry is estimated to account for about 7.2% of the total GDP of the Philippines, close to the approximately 10% GDP share of the entire primary industry in the Philippines, highlighting the important position of the gaming industry in the economic development of the Philippines.

The gaming industry can receive a certain degree of government support due to its ability to provide considerable fiscal revenue. According to data publicly disclosed by the Philippine Ministry of Finance in 2020, the total fiscal revenue of the Philippines was approximately 2.85 trillion pesos (including tax and non-tax revenue), of which PAGCOR contributed about 30 billion pesos in taxes and non-tax funds, ranking third after the Bureau of Internal Revenue (BIR, hereinafter referred to as BIR) with 1.95 trillion pesos and the Customs with 0.53 trillion pesos.

The Philippine government imposes a 5% franchise tax on such casinos based on their GGR (Gross Gaming Revenue) amount, and the gaming revenue of such casinos is not subject to corporate income tax. However, non-gaming revenue within venues such as Manila International Entertainment City is subject to a 30% income tax. There are three types of gaming taxes for gamblers: one is a gaming tax for the general public, with a tax rate of 25%; one is a gaming tax for local VIPs, with a tax rate of 17%; and the third is a gaming tax for foreign VIPs, with a tax rate of 15% (Zeng Zhonglu, 2022). Additionally, Philippine offshore gaming operators (POGO, hereinafter referred to as POGO) are also subject to a franchise tax, which was previously 2% and is now 5%.

As a state-owned enterprise, PAGCOR not only regulates but also operates casinos, closely related to national development, contributing considerable taxes and non-tax funds. According to PAGCOR's annual report, 5% of its revenue is allocated as a franchise tax to the BIR; after deducting the franchise tax, 50% of the revenue is allocated as the statutory income share of the national government to the Ministry of Finance, and within this 50% government share, fixed or proportional funds are provided to government agencies such as the Philippine Dangerous Drugs Board (DDB), the Philippine Sports Commission (PSC), the Philippine Health Insurance Corporation (PhilHealth), and the Philippine Department of Justice Claims Commission.

In addition to fixed remittances to various government entities, PAGCOR, as a state-owned gaming company, also actively implements significant corporate social responsibility projects under its current management and leadership.

2. Current Development of the Philippine Gaming Industry

Apart from lottery and other businesses, the modern development of the Philippine gaming industry is inseparable from PAGCOR. The agency's charter shows that PAGCOR is entrusted with the following three tasks: to regulate, operate, authorize, and license card games and digital games, as well as casino games in the Philippines; to generate revenue for the Philippine government's social, civic, and national development plans; and to help promote the development of the Philippine tourism industry.

The Philippine gaming industry studied in this article specifically refers to the onshore and offshore gaming businesses under PAGCOR's regulation. Overall, it is believed that the current Philippine gaming industry can be divided into the following three major segments.

2.1 PAGCOR-operated Casinos

Unlike Macau, where the government regulates and enterprises manage themselves, PAGCOR is responsible for both regulation and direct operation of casinos. However, because PAGCOR plays the seemingly contradictory roles of regulator and operator, it has been questioned by Congress or the Ministry of Finance over the years, and discussions on the privatization of self-operated casinos have taken place. In August 2016, under the indication of then-President Duterte, PAGCOR announced for the first time its intention to sell its 47 casinos at the time, aiming to raise funds for the national budget, but the plan was later shelved.

At a Philippine Senate hearing on August 30, 2022, the new PAGCOR Chairman and CEO Alejandro Tengco stated that privatizing the agency's casinos might be the most reasonable development direction for the Philippine gaming regulatory agency, allowing it to focus on a single task. This also means that the future of self-operated casinos may change, which is worth continuous attention.

Currently, PAGCOR operates 9 branch casinos and 32 satellite casinos under the brand name "Casino Filipino," but focuses on small and medium-sized casinos with a single gaming function, located in Manila, Cebu Island, Mindanao Island, etc. Before the operation of large licensed casinos, self-operated casinos contributed the majority of gaming revenue.

2.2 Onshore Licensed Casinos

The so-called onshore licensed casinos refer to PAGCOR attracting domestic and foreign gaming entertainment companies or capital to enter the Philippines, issuing licensable licenses, and developing single or integrated projects that combine casinos, resorts, and shopping. In these aspects, it is not difficult to see the shadow of Macau.

Originally monopolized by Macau Entertainment, the government ended the monopoly and opened up gambling licenses in 2002, allowing foreign large entertainment groups to enter and build resort-style casinos. The Cotai Strip was also built in Cotai, imitating Las Vegas, gradually forming a gaming entertainment integrated resort city. Additionally, with the mainland's Individual Visit Scheme, Macau quickly became a world-class gaming tourism city.

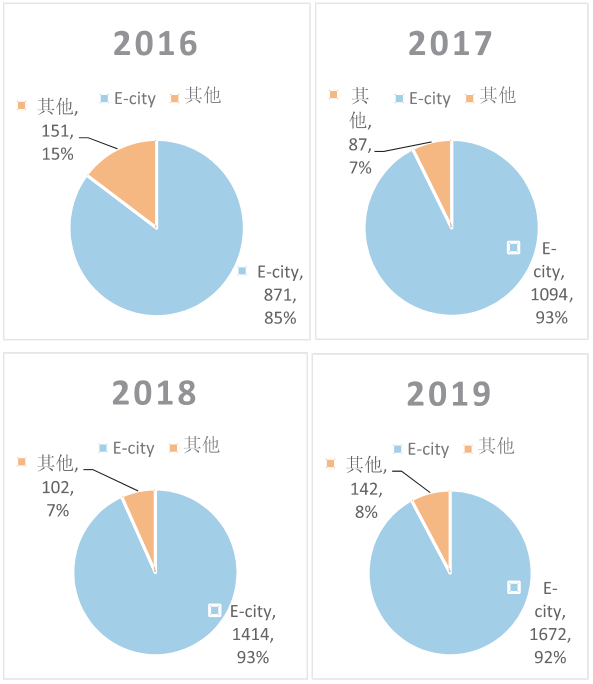

In the Philippines, with the opening of the first gaming entertainment integrated project, Resorts World Manila, in 2009, capital or gaming entertainment enterprises from local, Macau, Japan, and other places have successively entered over the next decade, starting a new chapter for Philippine physical casinos. The most representative is the Manila International Entertainment City (E-city) area, which includes the aforementioned Resorts World Manila, as well as the currently operating Solaire, Okada Manila, and City of Dreams Manila, these three large gaming entertainment complexes. There are also small and medium-sized licensed casinos distributed in the Manila Bay and Clark Freeport Zone areas.

Before the pandemic, the operation of onshore licensed casinos was generally good. According to data from 2016-2019, their GGR (Gross Gaming Revenue) accounted for 64% to 70% of the total GGR of the Philippine gaming industry. More specifically, only E-city generated GGR accounted for more than 90% of the total GGR of onshore licensed casinos (see Figures 1 and 2).

2.3 Offshore Gaming

The internet has expanded into almost every area of modern life, and gaming is no exception (Lamoste, A.D. & Prasetyawati, Y.R., 2021). The Philippines started offshore gaming earlier than its neighbors, but compared to onshore physical gambling, it appears more tortuous and chaotic.

First, it is necessary to mention the First Cagayan Leisure and Resort Corporation, a U.S.-listed company headquartered in Cagayan Province, Philippines, established in 2003, claiming to be the earliest legal offshore gaming license issuer in Asia. In fact, this company is merely equivalent to a paid service intermediary. Without direct government regulation, the Philippine government once granted it the authority to authorize (i.e., issue licenses) and supervise offshore gaming operators, basically allowing it to develop freely. During this period, various offshore gaming operators who obtained First Cagayan licenses or simply operated illegally began to appear in large numbers. Subsequently, issues such as drugs, money laundering, and organized crime began to accompany offshore gaming, harming the host country and surrounding regions. Since 2016, offshore gaming operators have rapidly developed in the Philippines, operating in a business process outsourcing (BPO) model (Moran, D.I, 2021).

Relevant enterprises took advantage of the Philippines' lenient gaming laws, targeting Chinese customers, making China the country most affected by this. A large number of Chinese people went to the Philippines to engage in illegal cross-border offshore gaming, and a large amount of capital began to flow into the Philippines, leading the Chinese government to repeatedly demand that the Philippines ban and crack down on illegal offshore gaming.

Due to the severity of illegal offshore gaming proliferation, in 2016, PAGCOR announced that the agency was responsible for legally issuing offshore gaming licenses. If a license was not applied for from PAGCOR, it would be considered illegal offshore gaming, leading to the decline of First Cagayan. However, in 2017, an incident involving government officials extorting a gaming operator for a license erupted, leading the Philippine Congress and the Supreme Court to accuse PAGCOR and demand a suspension of its offshore gaming license issuance business.

Amidst this chaos, another agency issued a statement claiming to be the only institution in the Philippines that could legally issue offshore gaming licenses, recognized by default by the Philippine Supreme Court, namely the "Asian Prestige Entertainment Cooperation" (APECO, which also attracted multiple reports at the time). However, just five months later, the government announced that APECO could only govern a specific small area, and the national legal offshore gaming license issuance authority returned to PAGCOR. Since then, the legal issuance and regulation of offshore gaming licenses in the Philippines have settled.

After resolving the regulatory issues, the Philippines began to address the illegalization of offshore gaming and balance tax issues. First, the existence of a large number of illegal offshore gaming operators meant a large number of illegal workers, followed by significant tax revenue losses and social security issues, with repeated reports of serious incidents such as kidnappings, causing domestic dissatisfaction. Additionally, because a large number of personnel illegally engaged in offshore gaming came from abroad, especially mainland China, this could easily damage bilateral relations. The Chinese government has repeatedly expressed opposition to offshore gaming, considering it harmful to China's interests and causing social problems.

Under the pressure of various internal and external factors, PAGCOR and relevant government departments have increasingly intensified their efforts to crack down on illegal POGOs. On the one hand, they continuously investigate and shut down illegal POGOs, such as on September 27, 2022, when the Philippine Department of Justice announced the closure of 175 offshore gaming companies whose licenses had been revoked but continued to operate illegally, deporting 40,000 Chinese employees. On the other hand, an independent supervisory team, CMED-IG, was established within the PAGCOR framework, and tax policies for offshore gaming were formulated, such as the enactment of Republic Act No. 11590 in September 2021, imposing a 5% tax on the GGR of POGOs.

These measures have played a role in combating and regulating illegal offshore gaming, but they have also impacted enterprises that legally hold POGO licenses. PAGCOR confirmed that among the 60 legal POGO operators it issued, only 27 are still actively operating, with some operators moving to countries with lower taxes, such as Vietnam and Laos.

In addition to the aforementioned issues, the former offshore gaming regulatory agency, PAGCOR, still does not wish to completely undermine offshore gaming. At least for legal and compliant enterprises, support should be maintained to obtain a lasting and stable source of tax revenue.

3. The Direction of the Philippine Gaming Industry Under the Impact of the COVID-19 Pandemic

Due to the severe impact of the COVID-19 pandemic, the global economic landscape has undergone significant changes, and the effects continue to persist. The Philippine gaming and tourism industries have also been severely affected. In the most severe year of 2020, the total GGR (Gross Gaming Revenue) of the Philippines plummeted to approximately 98.8 billion pesos, regressing to levels before 2014. During this period, the gaming industry suffered heavy losses due to the closure of some casinos, personnel capacity restrictions, and a significant decline in overseas tourists, while the government also faced great pressure due to increased foreign debt, pandemic control pressures, and rising unemployment rates.

Against this backdrop, the Philippines adopted two strategies: market innovation and policy adjustment:

First, PAGCOR