In recent days, the decentralized cryptocurrency 'casino', the prediction platform Polymarket and the contract exchange Hyperliquid, have revealed two significant vulnerabilities.

Polymarket— The Will of the Community Hijacked

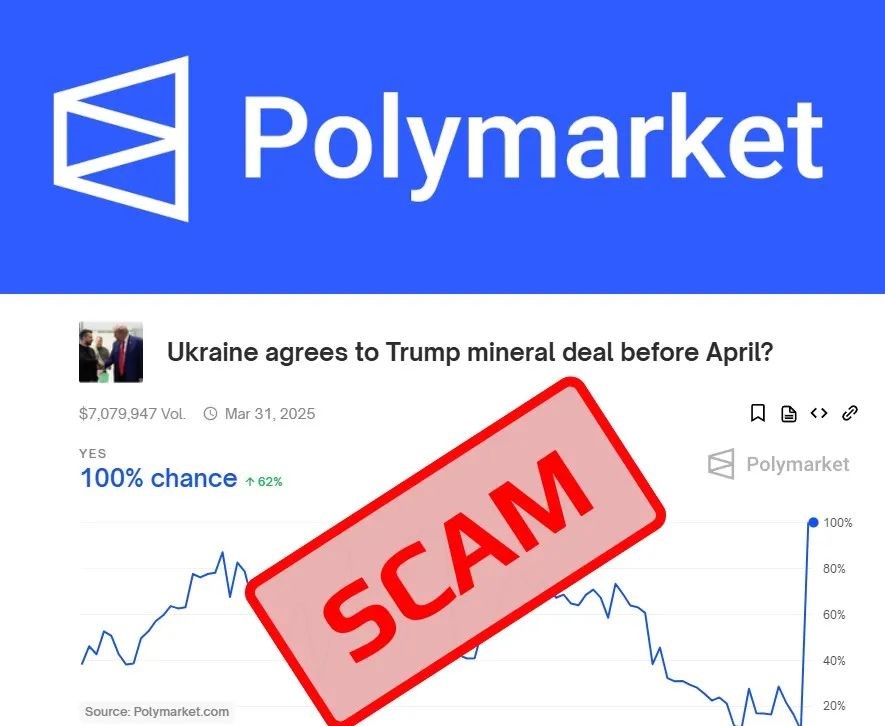

On Polymarket, the market predicting the completion of a rare earth agreement between Trump and Ukraine before April experienced an absurdly premature settlement. A whale gambler, who was about to lose money, manipulated the possible facts through the operation of arbitration rights (UMA community governance) and achieved a winning market outcome. This has sparked widespread discussion in the internet community.

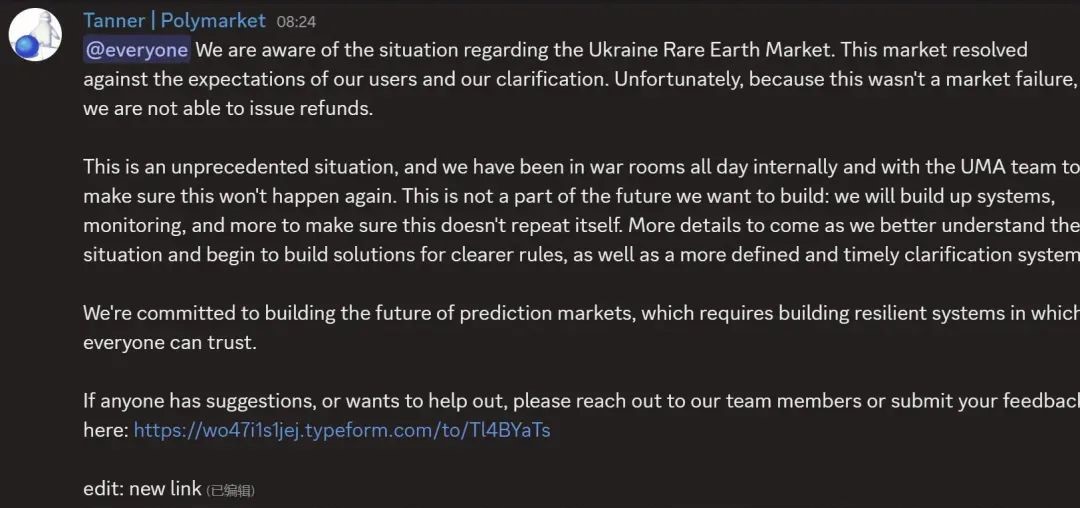

After the incident, Polymarket's official announcement acknowledged the loophole but refused to change the result. They believe it was not a market error but an action within the rules, refusing to intervene in the outcome. They will strengthen cooperation with the UMA team to prevent similar incidents.

To understand this incident, it is necessary to briefly organize the operation mechanism of Polymarket, a decentralized prediction market that bets money on the outcomes of future events. The entire design is transparent, and the final result determination is entrusted to a credible data source, requiring the introduction of a decentralized 'oracle' system to verify the authenticity of the settlement results in reality.

The 'oracle system verification' serves as the authority on event judgment, responsible for feedback on real data. The blockchain is closed, the internet is open, and this oracle function can be likened to bridging information.

The bridging tool used by Polymarkets is provided by the UMA (Universal Market Access) protocol. The UMA protocol offers an 'Optimistic Oracle' system, which verifies data in a 'true unless disputed' model and arbitrates disputes through UMA token holder voting when necessary.

By default, the 'oracle's' judgment is accepted. If someone disputes the result, it enters a dispute arbitration phase, where UMA token holders vote to decide the settlement, with this whale gambler hijacking the arbitration rights of UMA tokens.

Dispute Part Introducing Arbitration Rights (UMA Community Governance)

When a market event on Polymarket ends, anyone can propose a result ('yes' or 'no') and submit it to the UMA oracle for verification.

The submitted result enters a challenge period (usually 2 hours). During this period, if someone believes the proposed result is incorrect, they can pay a deposit (usually 750 USDC) to raise a dispute.

If the result is disputed twice, the issue is handed over to UMA's data verification mechanism (DVM), and the final result is decided by a vote of UMA token holders. The size of the voting rights is proportional to the amount of UMA tokens staked by the holder.

If you want to propose a market settlement result on Polymarket, you need to pay 750 USDC as a deposit. If your proposal is not disputed or ultimately proven correct, you will get back this deposit and receive an additional reward (usually 5 USDC). If the proposal is wrong and successfully disputed, you will lose this deposit. Similarly, the person raising the dispute also needs to pay 750 USDC. If the dispute is successful, the disputant can obtain the proposer's deposit as a reward; if it fails, they lose their own deposit.

To participate in UMA's voting, you need to stake UMA tokens in UMA's voting application (vote.uma.xyz). The amount of UMA staked determines your weight in dispute voting

The cost of disputing twice is approximately 1500 USD (750USDC*2), which generally deters ordinary gamblers. At the same time, the majority holding UMA tokens; typically, a major holder in a market risk arbitrage scenario, it's impossible to lose under the rules.

Polymarket's prediction market currently has many potentially disputable Market—Submissions, which may ultimately change the results through voting rights. It's just that previously, the amounts involved or the facts might have room for interpretation, and the issue fizzles out; the market that exploded was just too brazen in its operations.

Hyperliquid Incident— Platform Pulls the Plug for Self-Rescue

Hyperliquid is a decentralized perpetual contract exchange known for its efficient trading experience and high leverage features. Its native token is $HYPE, and the platform has a liquidity pool called Hyperliquidity Provider (HLP), responsible for taking over counterpart positions.

The trading target is a meme coin $JELLY based on Solana, launched by Venmo co-founder Iqram Magdon-Ismail in January this year, related to the Web3 social media project JellyJelly. The market value of this token was initially between 10 million and 20 million USD, classified as a small token with low liquidity.

The incident started when a trader (wallet address suspected to be 0xde95) opened a massive short position of at least $500 on Hyperliquid against $JELLY, with a leverage of up to 20 times. Subsequently, this trader was suspected of deliberately driving up the price of $JELLY through on-chain operations.

Within one hour, the price of $JELLY surged by 230%, even reaching a peak increase of 429%. This led to the liquidation of the trader's short position. Due to the large size of the position, Hyperliquid's HLP liquidity pool automatically took over this part of the short position, becoming the passive short side.

As the price of $JELLY continued to be pushed higher (once nearing 0.16 USD), the unrealized losses of the HLP rapidly increased, reaching approximately 10.6 million to 13.5 million USD. If the price further rose to 0.17 USD, the losses could expand to 240 million USD, threatening the stability of Hyperliquid's entire capital chain.

Hyperliquid's validator committee (an autonomous organization responsible for voting decisions) quickly convened a meeting, citing 'suspicious market activity' as the reason, and voted to delist the perpetual contract trading of $JELLY, forcibly settling all related positions at 0.0095 USD. This price was far below the market price at the time, effectively avoiding greater losses, but also sparked controversy.

Hyperliquid's platform net outflow exceeded 140 million USD of USDC, and Hyperliquid's native token $HYPE dropped about 10% to 20% within 24 hours, falling below 15 USD at its lowest.

Market Manipulation Allegations

Many believe that this trader exploited the low liquidity of $JELLY, first opening a short position on Hyperliquid (DEX), then pulling the market on the spot market, forcing HLP to take on huge losses, in a well-planned short squeeze. (This kind of shorting is essentially sabotaging the enterprise)

While Hyperliquid delisted $JELLY, Binance and OKX announced the launch of perpetual contract trading for $JELLY, causing its price to soar further.

The incident exposed the vulnerability of decentralized trading platforms to market manipulation when dealing with low liquidity tokens and high leverage trading.

Hyperliquid (DEX) avoided greater losses through decisive action, but its centralized decision-making model and high-risk design (unrestricted position size and mixed vault for small tokens) have been widely criticized.

Monetary Power

The Polymarket incident is a classic case of exploiting rules to 'steal crystals'.

The most classic precedent for the Hyperliquid incident is the 2021 GameStop short squeeze.

The commonality of both incidents is that monetary power can coerce the market, with the Polymarket incident manipulating arbitration (governance environment) to distort the outcome. The Hyperliquid incident targeted low liquidity tokens with high leverage to exploit the platform.

Polymarket's product does not have the final interpretation right, only respecting the results within the game rules, with the only guarantee being the enhanced monitoring of arbitration rights.

Hyperliquid's product retains the final interpretation right, ensuring they do not go bankrupt due to high-risk design. For business owners facing financial crises, pulling the plug to break the crisis is not a wrong choice. In the real world, face is given by others, but the substance is one's own.

Influential Bugs May Also Be a Form of Marketing

In product design, we often pursue perfection, but in reality, influential bugs are indeed an effective form of marketing.

From a human nature perspective, people like to promote products that are profitable for them. The pursuit of profit is inevitably a bug in human nature.

Currently, Polymarket still has quite a few registered accounts each month, many of which are prepared for the site's airdrop gambling. After the US presidential election, Polymarket's popularity has also declined in recent months.

At the same time, they have very strict measures for high-frequency trading users.

Hyperliquid's operating model is very adept at gambling against retail investors, with the majority of situations being advantageous to one side. The majority of retail contract blow-ups are typical. The unlimited position size is also a form of marketing, just not expected to be backfired, forced to exercise the final interpretation right (forced liquidation), letting users share the cost.

Finally, returning to the article's theme, is it still possible for a decentralized 'casino' to achieve absolutely fair results?